Smartphone and tablet stats: what's really going on in the mobile market?

By Speedway

on

Thursday, August 11, 2011

with

The mobile phone market is deluged with data. Four times a year there is a spike in market share estimates just after quarterly financial results are released, while the time in between is filled with analyst forecasts and surveys from market research firms trying to get to the bottom of changing market trends.

IDC describes this as a "transition point", and is backed up by US market research firm Nielsen, which claims that in its home market, more smartphones were sold between March and May 2011 than feature phones. However, the transition point is not just happening in big Western markets: IDC notes strong sales of low-cost Android smartphones in Latin America, and also in south east Asia.

The company's tale of the top five mobile phone vendors shows Nokia still in first place, having shipped 88.5m units, but with its market share having fallen from 33.8% in Q2 2010 to 24.2% in Q2 2011. That raises the spectre of second-placed Samsung (70.2m units / 19.2% market share) overtaking it in the near future.

Smartphone shipments

That's for all phones, but many app developers are focusing purely on smartphones. There is no shortage of estimates for that sector of the market in the second quarter of this year, and some hard data too.

Starting with the latter, Apple sold 20.4m iPhones in Q2, overhauling Nokia, which sold 16.7m "smart devices" – the term it uses for smartphones. HTC has just announced that it sold 12.1m smartphones in Q2, while other companies revealing their smartphone figures include LG (5.4m), Sony Ericsson (5.3m), Motorola (4.1m).

Samsung and Research In Motion are a bit more awkward. In the former case, it's because Samsung declined to give exact figures for its smartphone sales in Q2, citing competitive fears. In RIM's case, the difficulty is that its financial year doesn't follow the calendar year, so in its fiscal quarter ending on 28 May, it shipped 13.2m BlackBerry smartphones. Analyst ABI Research has provided predictions for both, pegging Samsung's Q2 smartphone shipments at around 19m, and sticking with RIM's figure of 13.2m.

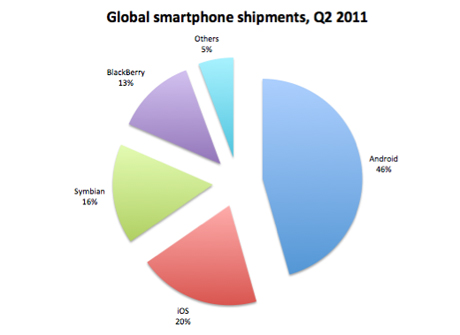

Divvying smartphone shipments up by manufacturer is one thing, but what app developers are more interested in is the operating system split. ABI Research thinks Android took a 46.4% share of smartphone shipments in Q2 with 47m units, ahead of iOS (20.4m), Symbian (16.7m) and BlackBerry (13.2m).

Source: ABI Research

Source: ABI Research Smartphone penetration

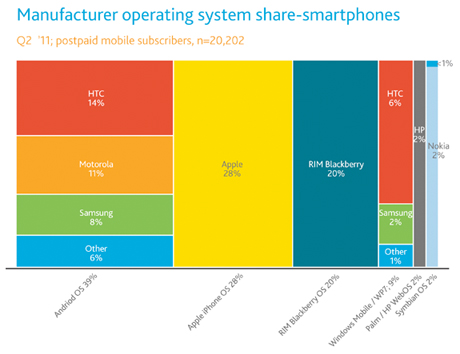

The data above applies to new shipments of smartphones, but there are other companies looking into how many devices each OS has out in the wild. Nielsen has just published a handy chart tracking OS share among smartphone owners with a contract in the US, for example.

It puts Android's share at 39%, followed by iOS (28%), BlackBerry (20%) and then Windows Mobile and Windows Phone combined with 9%. Android and Windows Phone penetration is also broken down by manufacturer, which is useful.

Source: Nielsen

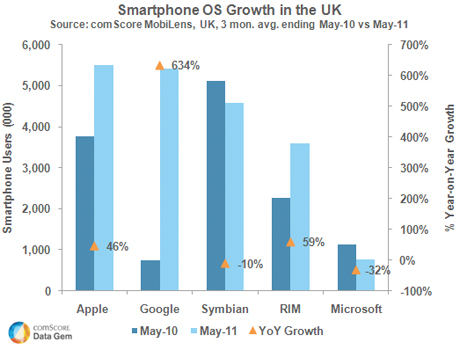

Source: Nielsen comScore caused controversy in July 2011 with its own estimates for smartphone OS penetration in the UK, which suggested iOS has a 27.1% market share, followed by Android (26.7%) and Symbian (22.5%), with BlackBerry some way behind.

Research In Motion complained publicly about these stats, however, saying that while comScore estimates it has 3.6m BlackBerry users in the UK, the actual figure is just under 7m.

Source: comScore

Source: comScore Smartphone and apps predictions

What about the future, then? Or at least the near future. Analyst firm Gartner has made its predictions for sales of smartphones to end users – note, this is different from shipments, since it covers phones actually being bought by people, as opposed to being stocked by retailers.

It sees Android taking a firm grip of the market this year running right through to 2015, when Gartner thinks Google will be powering just under half (48.8%) of all smartphones sold. The company thinks 467.7m smartphones will be sold in 2011, rising to 1.1bn by 2015.

But the key point is that it thinks this will continue to be a four-horse (at least) market, with Windows Phone (19.5% in 2015), iOS (17.2%) and BlackBerry (11.1%) all having healthy sales bases for the next four years. Yes, it's easy to scoff at any company making bold predictions for the next four years of a market that's changed hugely in the last four years – Apple's iPhone is four years old after all.

The obvious follow-on from these predictions are estimates for how app developers will benefit. Canalys has some forecasts on this front, claiming that direct revenues from sales of apps, in-app purchases and app subscriptions will top $7.3bn (£4.4bn) in 2011, rising to $36.7bn (£22.3bn) by 2015. These estimates do not include advertising revenues.

Strategy Analytics thinks that by the end of 2012, paid downloads will reach nearly $2bn every quarter, with Android Market overtaking Apple's App Store for the volume of downloads (but not the revenues) by the end of that year too.

Meanwhile, IDC has its own research into apps, albeit with figures for the number of downloads rather than revenues. It thinks that mobile app downloads will rise from 10.7bn in 2010 to 182.7bn in 2015, with social and location features contributing to a shift away from paid download revenues towards in-app purchases and advertising.

Tablet sales / predictions

The last area experiencing some frenetic number-crunching in July was the tablet market, both in terms of what's selling now, and what will be selling in the rest of 2011 and beyond.

Strategy Analytics recently published its estimates for Q2 2011, claiming that Apple's iPad took a 61% share of tablet shipments with 9.3m units, with Android nabbing a 30.1% share with 4.6m. The company thinks 0.7m Windows-powered tablets edged RIM's BlackBerry PlayBook (0.5m) into fourth place in the tablet OS market.

Separately, investment bank UBS predicts that iPad will take a 63% share of the tablet market for 2011 as a whole with 37.9m units, although it divides the market by manufacturer rather than operating system. That sees Samsung in second place with 5m sales, followed by Asus (2.2m), RIM (1.9m) and Motorola (1.8m).

Informa Telecoms & Media also has its crystal ball working overtime on tablets, suggesting that iPad currently has 75% of the market, but that this will fall to 39% in 2015, just ahead of Android's 38% – Informa thinks 90m iPads and 87m Android tablets will be sold that year, with Android finally overtaking iOS in 2016.

Lies, damned lies and statistics? Quite possibly: this can only be a snapshot of what people think is happening in the market. Expect many of these predictions to be revised during the second half of 2011, as the smartphone and tablet markets continue their dizzying evolution.

Category: Featured

Enter your email address below to receive updates each time we publish new content..